Lump sum lifetime mortgage vs drawdown lifetime mortgage

Lump sum lifetime mortgage

A lump sum lifetime mortgage is where you receive all the money you release in one go and there are typically no monthly repayments to make unless you choose to as the loan, plus compound interest, is typically repaid through the sale of the property when the last remaining applicant passes away or moves into long-term care. Alternatively, if you opt for a Horizon Interest Reward lifetime mortgage, monthly interest payments are required for an agreed term of 5, 10 or 15 years in order to obtain a discounted interest rate.

With our lifetime mortgages you could release from £15,000 to £1.5 million, depending on your personal circumstances.

When you complete your lifetime mortgage, you’ll receive all your tax-free cash in a single lump sum. This can be ideal if you have several expenses to cover at once, such as repaying an existing mortgage, gifting to a family member and home improvements. A lump sum lifetime mortgage could cost more over time as interest is applied to the full release amount from day one.

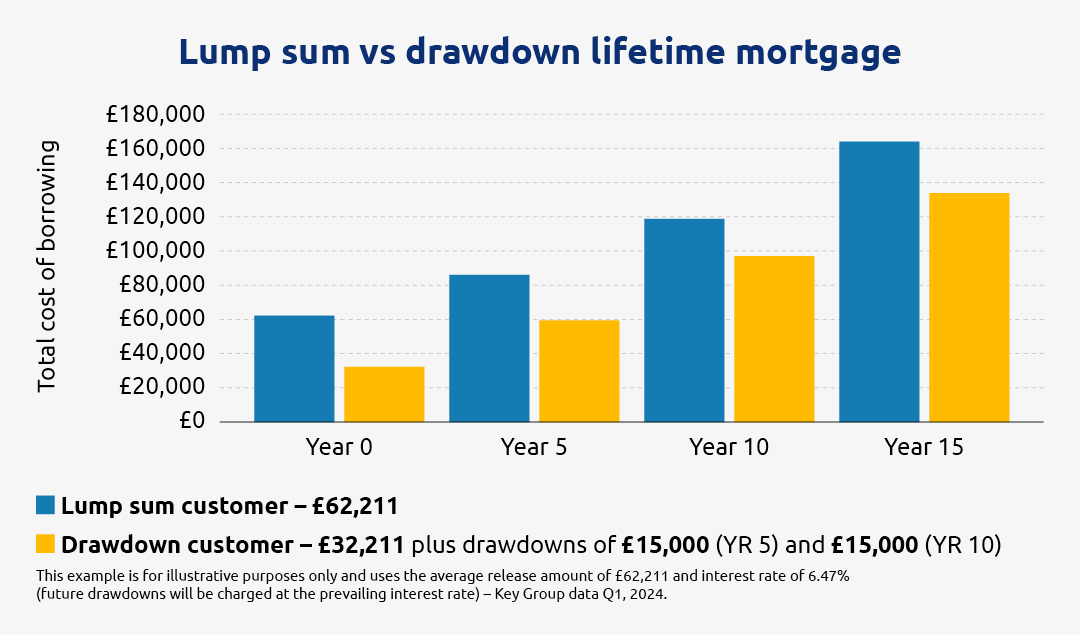

Drawdown lifetime mortgage

With a drawdown lifetime mortgage, you still get access to tax-free money and again there are typically no monthly repayments to make unless you choose to.

However, instead of receiving your funds in one lump sum, you can take the money as and when you need it following an initial release of at least £15,000.

This could be suited to you if you don’t need all your money upfront and want access to cash later down the line. It could also work out cheaper – as you only pay interest on the money you release and at the time you receive it, meaning you’re not paying interest on cash you don’t need.

It’s worth noting, though, that the interest rate applied to any drawdowns you make will be the prevailing rate at the time, not the rate you initially secured. A drawdown facility is not guaranteed as the lender has the right to withdraw it.

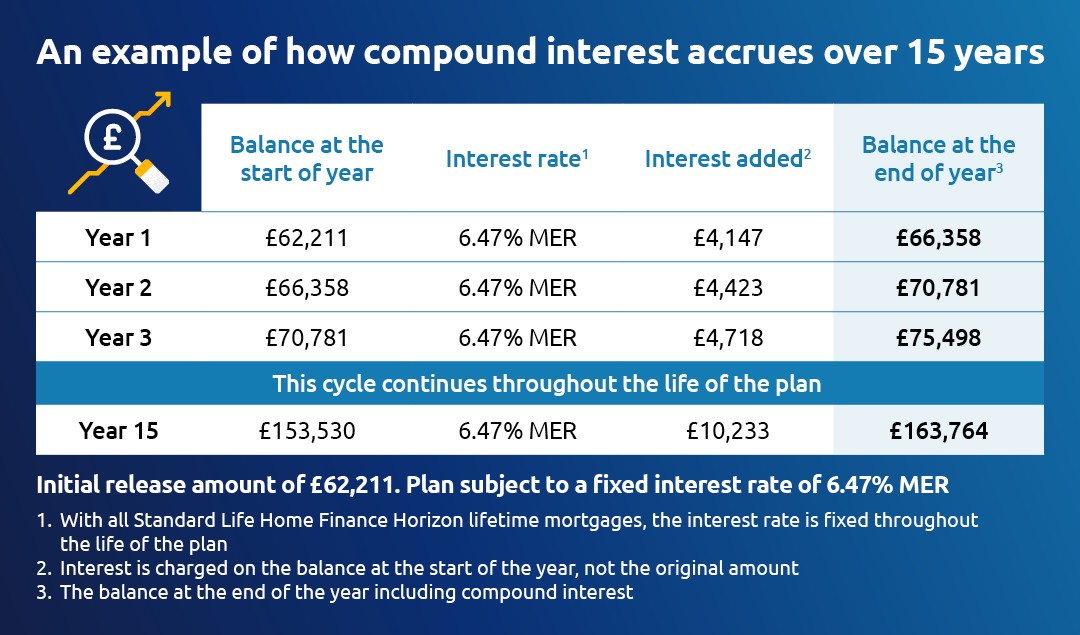

How compound interest affects your lifetime mortgage

There are typically no monthly repayments to make on a lifetime mortgage unless you choose to. As a result, you are charged interest not only on the loan itself, but also the interest that’s already been accrued, otherwise known as compound interest. This will result in your debt growing bigger over time.

For example, at the end of the first month of your lifetime mortgage (or year, depending on your plan), the interest will be charged on the original amount that you borrowed. Following this, in the second month or year of your plan, and each period thereafter, the interest will be charged on the full balance of your loan, including any previous interest accrued at that time. This cycle continues until the plan comes to an end.

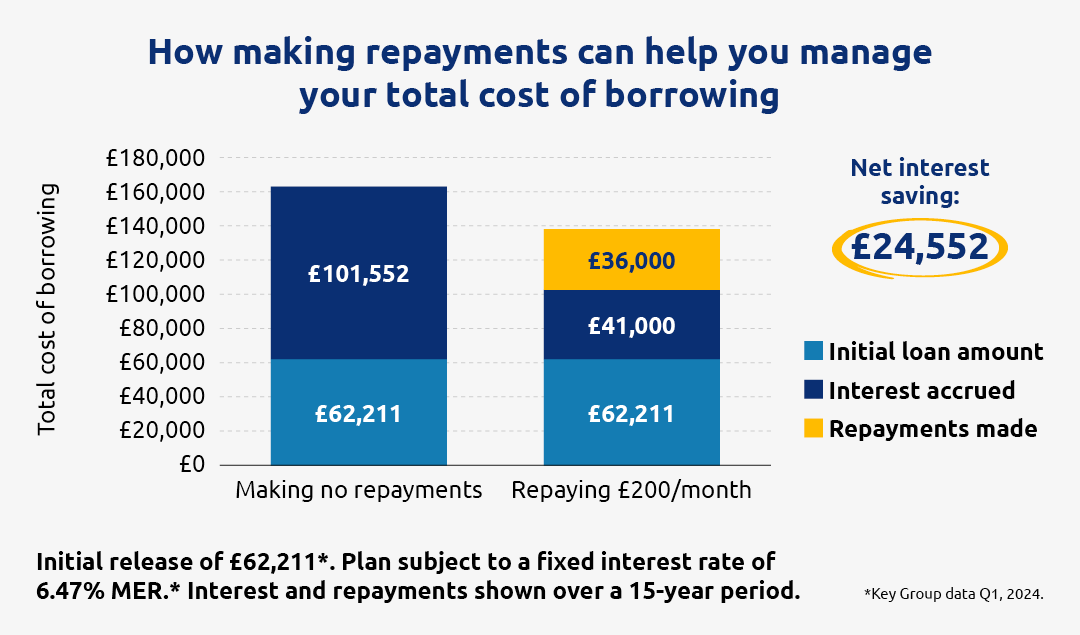

Reducing your cost of borrowing

Making ad-hoc or regular repayments

With all Standard Life Home Finance's Horizon lifetime mortgages, you have the option to make repayments, if you wish, without incurring early repayment charges, subject to criteria. We recommend that this is discussed with your equity release adviser to understand what would deliver the best outcome for your existing circumstances and future needs.

Considering a drawdown lifetime mortgage

Horizon Interest Reward

It’s important to discuss this with your equity release adviser and consider your affordability to make payments.

What to consider before taking out a lifetime mortgage

When considering equity release, we want you to be aware of the benefits and drawbacks before making a decision.

- You can unlock cash from your home, tax-free, to help meet your needs in later life

- You’ll always retain full ownership of your home and can stay in it for as long as you wish with a Horizon lifetime mortgage

- You can choose to make reduced or no monthly repayments to suit your circumstances with a Horizon lifetime mortgage, subject to criteria. Or with a Horizon interest reward lifetime mortgage you'll be rewarded with a discounted interest rate by paying off some or all of the interest each month over an agreed term of 5, 10 or 15 years

- You’ll never owe more than your home’s worth with a Horizon lifetime mortgage

- You may be able to remortgage your plan in the future to release further funds or secure a better interest rate, although this isn’t guaranteed and may be subject to early repayment charges

- A lifetime mortgage is a loan secured against your home and subject to compound interest, meaning the amount you owe can grow quickly

- Equity release will reduce your estate’s value and may affect your entitlement to means-tested benefits

- A lifetime mortgage may result in limited or no property equity remaining and will reduce your financial options in the future

- You should always think carefully before securing a loan against your home to repay existing debt

- The loan, plus compound interest, is typically repaid through the sale of the property when the last remaining applicant passes away or moves into long-term care

- An advice fee may apply. Advice fees vary among independent financial advisers, so we recommend discussing this with your adviser if you are unsure

- A lifetime mortgage is a long-term financial product and is not designed to be fully repaid until the death or entry into long-term care of the last remaining borrower, otherwise early repayment charges may apply

Getting the right advice

If you are considering a lifetime mortgage, it is a Financial Conduct Authority regulation that you first seek advice from a qualified equity release adviser, who will help you understand your options and advise on what is right for you.

All Equity Release Council members agree to abide by Equity Release Council rules, guidance and standards, and have signed up to the Council's Statement of Principles. When finding your equity release adviser, you can search the Equity Release Council's database of registered equity release adviser members.